Super Apps in Asia: The Digital Innovation Transforming Urban Life

In the last decade, Asia has become a global leader in mobile-first innovation. One of its most transformative contributions to the digital world is the emergence of the super app – a multifunctional mobile platform that allows users to shop, commute, pay bills, message friends, and access essential services, all in one place. Unlike in the West, where apps are siloed by function, the super app in Asia acts as a digital operating system for everyday life. From Tencent’s WeChat in China to Grab and Go-Jek in Southeast Asia, these platforms are reshaping urban living, economic activity, and digital infrastructure across the region.

- 1. What Is a Super App?

- 2. Market Leaders: The Big Names in Asia’s Super App Ecosystem

- 3. Why Super Apps Thrive in Asia

- 4. The Data Advantage: Personalization, Monetization, and AI

- 5. Economic and Social Impact of Super Apps

- 6. Challenges and Criticisms of Super Apps

- 7. Will Super Apps Expand Beyond Asia?

- Conclusion

1. What Is a Super App?

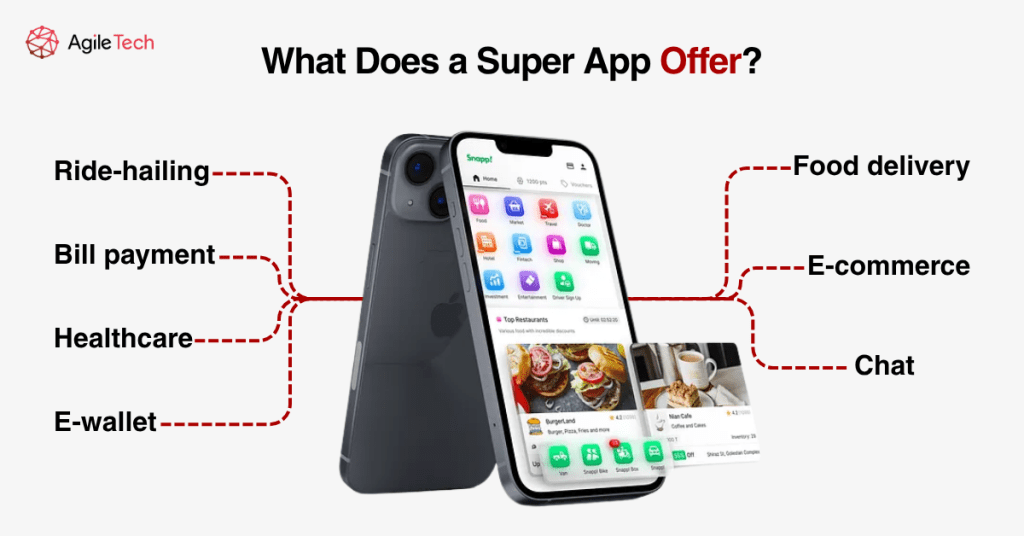

A super app is a mobile application that offers multiple services within a unified platform. Instead of switching between different apps for transportation, food delivery, payments, or messaging, users can complete all these tasks in a single interface. This eliminates friction and creates a more seamless digital experience.

Super apps act as operating systems for mobile users. By integrating key daily services, they turn the smartphone into an all-in-one tool for urban living, especially in densely populated cities like Jakarta or Ho Chi Minh City.

Some of the most common features included in super apps are:

- Instant messaging and social interaction

- Ride-hailing and delivery logistics

- Digital payments, wallets, and peer-to-peer transfers

- Online shopping and e-commerce

- Financial tools like insurance and microloans

- Health, government, and public services

The defining trait of a super app is not just its feature count, but the smooth interoperability between services, enabled through data and platform integration.

2. Market Leaders: The Big Names in Asia’s Super App Ecosystem

2.1 WeChat: The Pioneer of Super Apps

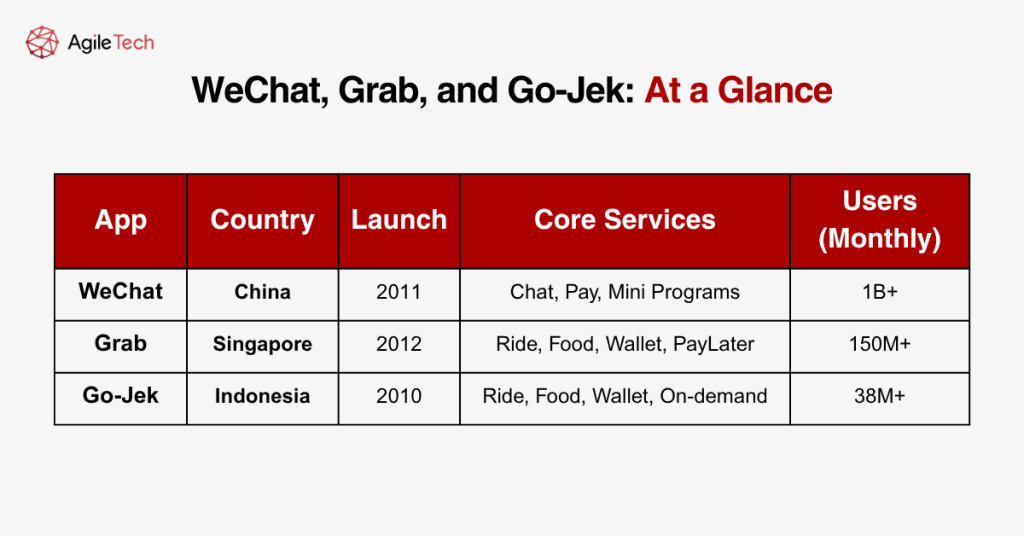

WeChat, created by Tencent in China, has become the blueprint for super apps globally. What started as a messaging tool has grown into a digital ecosystem with over 1 billion monthly users. It integrates services that span from social feeds to mobile payments and even medical booking.

The most transformative aspect of WeChat is its “Mini Programs” apps within the app that let users order food, pay bills, play games, and access services without leaving the WeChat environment.

2.2 Grab: Southeast Asia’s Multi-Service Powerhouse

Grab began as a ride-hailing startup in Malaysia and has expanded into eight Southeast Asian markets. Its evolution into a super app reflects the region’s needs, combining transport, finance, delivery, and more in a single platform.

Today, Grab supports users with:

- Ride and delivery services (GrabBike, GrabCar, GrabFood, GrabExpress)

- Financial tools like GrabPay and PayLater

- Merchant services for local businesses

- Healthcare, insurance, and hotel bookings

Grab’s integration with local governments and partnerships with SMEs have helped it build a strong foundation for inclusive digital growth.

2.3 Go-Jek: Indonesia’s Inclusive Innovation Engine

Go-Jek launched in Jakarta to connect motorbike taxis with customers. Since then, it has transformed into an Indonesian super app offering over 20 services across transport, lifestyle, finance, and on-demand labor.

Popular Go-Jek offerings include:

- Go-Ride and Go-Car for urban transport

- Go-Food for food delivery

- Go-Massage and Go-Clean for personal services

- GoPay for digital payments and peer transfers

Go-Jek stands out for its mission to empower micro-entrepreneurs, especially informal sector workers who lack access to formal employment.

Read more: Super App: 5 Examples of Super Apps Successful Case

3. Why Super Apps Thrive in Asia

Asia offers a uniquely favorable environment for super apps to flourish. Rapid urbanization, mobile-first behavior, and infrastructural challenges make bundled digital services more efficient and attractive than stand-alone apps.

Large cities in Asia are densely populated, with inefficient transport and service delivery. Super apps help streamline everyday tasks, reducing friction in commuting, paying, ordering, and communicating—all through one interface.

Moreover, smartphone penetration is high while traditional desktop access remains limited. This has led to a mobile-first internet culture, where super apps become default gateways to the digital economy.

Another key driver is the region’s large underbanked population. Many people lack access to credit cards or banking, and super apps have bridged this gap with digital wallets, mobile top-ups, and micro-finance features that are easy to use and quick to access.

Lastly, the region’s youthful demographic, especially Gen Z and millennials, demands instant gratification. Super apps deliver just that, combining speed, accessibility, and convenience in one tap.

4. The Data Advantage: Personalization, Monetization, and AI

Super apps collect enormous amounts of behavioral data. This includes users’ movement patterns, spending habits, search history, and even social preferences. Such granular data allows for highly personalized experiences and deeper engagement.

With this insight, platforms can fine-tune service recommendations. For example, if a user regularly orders food on weekday evenings, the app may offer time-sensitive meal deals or suggest new restaurants based on past choices.

This data-driven approach also benefits businesses. Partner merchants can access user trends, optimize marketing campaigns, and track conversions in real time, something traditional advertising rarely achieves at this scale.

On the backend, super apps deploy artificial intelligence to streamline operations. AI powers chatbots, fraud detection, dynamic pricing, and even financial scoring. These tools reduce costs and improve customer support at scale.

As AI capabilities grow, super apps will likely evolve into predictive digital assistants, capable of anticipating user needs, automating decisions, and delivering hyper-personalized services.

5. Economic and Social Impact of Super Apps

Super apps play a crucial role in job creation. From delivery drivers and riders to freelance service providers and resellers, the platforms enable millions to earn income with minimal barriers to entry.

This impact is especially strong in emerging economies. Informal workers who lack access to job security or capital can now monetize their labor directly through the app, often with the added benefit of micro-insurance or credit.

In addition, small and medium enterprises (SMEs) benefit from the infrastructure of super apps. Without building their app, local merchants can reach customers, accept digital payments, and run loyalty campaigns through the platform.

Examples include street food vendors using Go-Food to manage orders or tailors using GrabExpress to handle deliveries. These integrations bring traditional businesses into the digital economy with minimal investment.

Super apps also contribute to financial inclusion. Digital wallets like GoPay or GrabPay allow people without bank accounts to make secure payments, send money, and access essential financial services.

6. Challenges and Criticisms of Super Apps

As super apps gain prominence across Asia, concerns about their long-term impact on privacy, competition, and digital equity are growing. While these platforms offer convenience and economic value, they also introduce complex risks that require careful regulation and ethical responsibility.

6.1 Data Privacy and Security Concerns

Super apps handle massive amounts of personal data, from users’ real-time locations to their financial transactions and communication history. In regions where data protection laws are weak or outdated, users are often unaware of how their information is collected, stored, or monetized. This lack of transparency raises serious concerns about surveillance, consent, and the vulnerability of centralized data systems.

Moreover, security threats are escalating. As super apps become attractive targets for hackers, a single breach could expose millions of user records. The stakes are especially high when sensitive information like health data or payment credentials is compromised. Without a robust cybersecurity infrastructure, the promise of convenience may come at the cost of personal safety.

6.2 Platform Monopoly and Anti-Competitive Behavior

Super apps can unintentionally create digital monopolies. By bundling diverse services into one ecosystem, they make it difficult for smaller, specialized apps to compete. Startups often lack the resources to match the scale or incentives offered by these platforms, which stifles innovation and narrows consumer choice. This dynamic has triggered concerns about reduced competition and over-centralization of market power.

Some governments in Southeast Asia are beginning to examine these issues. Antitrust investigations and regulatory discussions have emerged in countries like Indonesia and Singapore, where platform dominance is becoming more visible. However, enforcement remains inconsistent, leaving many small businesses vulnerable to exclusion or algorithmic invisibility.

6.3 Overdependence on a Single Platform

For many users and merchants, super apps have become digital lifelines. However, this dependency comes with risks. If the platform experiences a technical failure or policy change, millions may lose access to essential services such as payments, transportation, or health consultations. The resulting disruption can paralyze business operations and daily routines.

Merchants relying heavily on a super app face similar risks. Changes in commission rates, visibility algorithms, or service policies can significantly impact their income overnight. This overdependence limits bargaining power and reduces autonomy, creating a fragile ecosystem where one platform holds disproportionate influence over the livelihoods of many.

6.4 Ethical and Labor-Related Criticism

The gig economy that powers super apps is often criticized for lacking worker protections. Many drivers, couriers, and service providers face irregular pay, limited benefits, and high commission fees. Without legal recognition or employment contracts, these workers are left with few avenues for support or dispute resolution.

While companies like Grab and Go-Jek have introduced programs like micro-insurance or upskilling, critics argue these are not sufficient. Long-term labor equity will require more comprehensive reforms, such as minimum wage standards, social insurance, and grievance mechanisms, to ensure that convenience for users does not come at the expense of worker welfare.

7. Will Super Apps Expand Beyond Asia?

While super apps dominate Asia, expansion into Western markets faces significant hurdles. Consumer habits in the U.S. and Europe tend to favor specialized apps that do one thing well. In contrast, Asia embraces convenience through integration.

Regulatory environments also differ. Western markets have stronger data protection laws and tighter antitrust scrutiny. This makes it harder for a single platform to bundle services without raising legal and ethical concerns.

Some companies are trying to replicate the model. Facebook has added payment features and business tools to Messenger. Uber offers food delivery, mobility, and financial services. But these remain siloed, and integration lacks the cohesion of WeChat or Grab.

Another barrier is ecosystem fragmentation. In the West, partnerships between banks, retailers, and tech firms are less centralized. This makes it difficult to build a seamless user journey under one brand.

Still, lessons from Asia are valuable. The success of super apps shows the power of ecosystem thinking, mobile-first design, and user-driven data personalization elements that any platform can adopt, even in different market contexts.

Read more: Agile Super App – Everything in One Touch

Conclusion

The super app is more than a mobile convenience; it is a foundational platform for economic development, social mobility, and digital transformation. In Asia, where smartphones are more accessible than bank accounts or desktops, these platforms have become a new layer of infrastructure. From WeChat’s digital empire to Grab’s inclusive financial tools and Go-Jek’s empowerment of micro-entrepreneurs, super apps represent the future of digital living, fluid, unified, and deeply localized.